As the world’s attention becomes distracted by wars and unrest, climate risks, chiefly due to flood and fire, loom. How will these risks affect households? And how can households prepare in advance?

When it comes to flooding, companies are distributing advice on the details of flood preparedness, and many municipalities subsidize flood mitigation programs.

Economists, however, are interested in the bigger picture: What are the macroeconomic implications of climate change and adaptation on housing in general?

“Physical risks directly impact house prices and lending and insurance decisions,” said Yasmine van der Straten, Assistant Professor in Finance at Nova School of Business and Economics.

Van der Straten was presenting a webinar on April 30, 2026, as part of the Virtual Seminar on Climate Economics (VSCE), a series organized by the Europe-based Centre for Economic Policy Research (CEPR).

Her research posed the questions:

- What is the direct effect of climate change on house prices?

- Can we adapt efficiently, given price signals?

- Are there any indirect feedback effects due to financial constraints?

Her model described the economic system of housing as a “general equilibrium framework with overlapping generations.” Although it may seem counter-intuitive, housing is a non-durable good, because it must be continually paid for in some way.

Although the economy is exogenously exposed to idiosyncratic physical climate risk, she noted that households must endogenously adapt, creating resilience against climate risk.

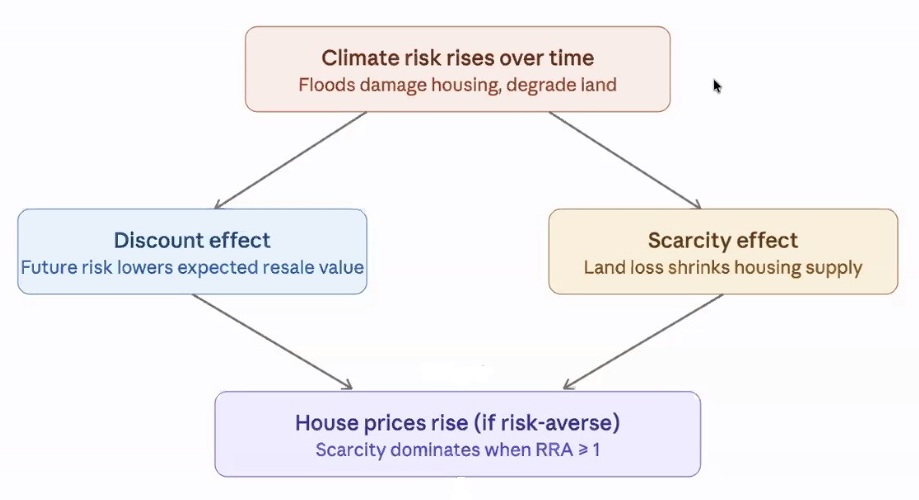

When it comes to housing, climate risk causes both a discount effect and a scarcity effect because physical climate risks lead to property damage and degrade the land, reducing the habitat available.”

According to the Intergovernmental Panel on Climate Change (IPCC), through landslides, erosion, desertification, etc., climate change degrades over a quarter of the Earth’s ice-free land. What was once good land will be abandoned after repeated flooding or droughts. “In the long term, land is in inelastic supply,” she said.

Households with positive savings lend to others. “Mortgage debt is backed by housing capital,” she noted, “and sufficiently large damages lead to what is known as an ‘underwater mortgage’, when you owe your lender more than your home’s current market value.” The model included household optimization.

“There is a direct effect,” she said, “when house prices are discounted because of exposure to future climate risk.” There is also a long-run effect, when “realized climate damages raise the shadow value of owning housing.”

In a single region, there are different housing stocks, as summarized by three houses in the thumbnail for this article.

“Differences in risk exposure generate price segmentation,” she said. “The relative price of safe housing rises as effective scarcity reallocates demand.” As land becomes scarcer, households build taller or denser, partially offsetting the land loss.

The researcher’s long-run simulation, which used the NASA Sea Level Projection Tool and is detailed in the paper, found that in 30 years, 64,000 homes in Florida would be at risk. By the end of the century, one million homes in Florida would be at risk.

Adaptation is not the same as insurance, van Straten emphasized. Adaptation reduces damage ex ante, whereas insurance compensates losses ex post.

Mortgage creditors anticipate climate risks. Financial constraints “lead to suboptimal adaptation” because such households underinvest in measures providing resilience. Moreover, she found that the “private adaptation gap” widens over time. Insurance leads to moral hazard in adaptation.

Conclusions

Climate risk lowers prices in physically exposed areas, while land scarcity increases the relative price of safer housing.

Forward-looking prices can incentivize efficient private adaptation (assuming frictionless markets).

Financially constrained households do not invest enough in resilience.

The private adaptation gap widens as households become more constrained.

The implication is that shifting toward landlord-based ownership can improve adaptation efficiency. ♠️

Click here to view the CEPR webinar “Flooded House or Underwater Mortgage?”