When it comes to forecasting liquidity risk, does your bank follow best practices? It might be tough to do so, because of a “data conundrum,” said Gudni Adalsteinsson, author of The Liquidity Risk Management Guide – from Policy to Pitfalls. Banks carry out a “retrospective analysis” on data that is “not forward looking.” Adalsteinsson, Head of Global Liquidity, Group Treasury at Legal & General Group Plc, was the first of three presenters on liquidity risk compliance, at a webinar on June 25, 2015, sponsored by the Global Association of Risk Professionals.

He praised the Basel III regulation on liquidity risk. It’s a “big step forward” because “it introduces the time element into the framework.” In an area that lacks standard definitions and methodology, Basel III is a sorely needed “first attempt to set the playing field,” he noted.

He praised the Basel III regulation on liquidity risk. It’s a “big step forward” because “it introduces the time element into the framework.” In an area that lacks standard definitions and methodology, Basel III is a sorely needed “first attempt to set the playing field,” he noted.

As an example of lack of data hampering good liquidity management, Adalsteinsson said that in a recent survey only about half of all banks were doing cash flow analysis in their liquidity management. He referred the audience to the PWC Balance Sheet Management Benchmark Survey.

“Basel III is an opportunity to get things right.” He urges banks to move away from seeing Basel III as just a “compliance exercise” and instead seeing it more as “an actual management tool.”

The success of Basel III is heavily linked to the quality of data and data systems. Instead of just reporting the liquidity compliance ratio (LCR), a good system will help the bank understand what lies underneath the number.

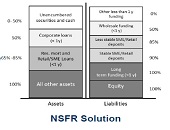

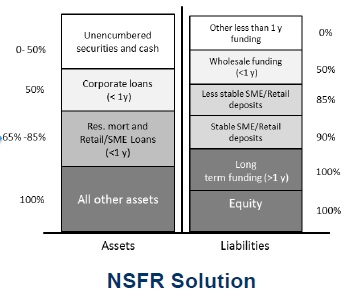

The net stable funding ratio (NSFR) is an important component of Basel III. Adalsteinsson said that inability to forecast the NSFR levels was a major drawback.

It all boils down to the longstanding problem of maturity mismatch, in which the long-dated liabilities are funded by short-term assets. “If you fail the test for NSFR, it will take eight years to get it right.”

Adalsteinsson likened the construction of an adequate framework to a recipe: it’s not just the ingredients, but also the order of combination that matters. His list of essential ingredients included cash flow projections, stress testing, and contingency planning, among other items.

He touched briefly on the 6-step framework which is described more fully in his book. At the heart of the framework is stress testing and the contingency funding plan (CFP). Risk managers must determine the stability of funding. “Risk is not black and white,” he said, “rather, it is 50 shades of grey.”

He gave an example of scorecard ranking on the Basel III groups, which might be too prescriptive. He showed an example of scenario stress testing, with a scenario of “sudden drop in market confidence” that yielded different survival rates, depending on the cut-off dates.

Adalsteinsson speaks from deep experience in the field. He was a group treasurer for an Icelandic bank during the 2008 financial meltdown, which offered him a front-row seat of liquidity risk management under severe crisis. ª

Click here to view the webinar presentation. Adalsteinsson’s portion is from slides 5 to 20.

Click here to read about the second presentation.

Figure 1 is from Adalsteinsson’s presentation.