Conference Call Tones. Part 2

Click here to visit Part 1. Interview with S. McKay Price, continued. Q: In the introduction to your paper on textual analysis of conference call tones, you describe a 2012 conference call in which David Einhorn grilled the management team of Herbalife, thereby causing the shares to fall 20 percent in price. Did you run the transcript of this conference call through your call tone algorithm, and if so, was it the most negative sample in the set? 2012 was not in our sample period so we did not specifically create tone measures for that Herbalife call. Although I suppose […]

Conference Call Tones. Part 1

“Spin,” said Morty. “It’s all about spin.” He pointed to the web interface where he was listening to a certain equipment manufacturing company try to explain anomalies in their reported expenses. Like hyenas, the analysts were picking apart the footnotes. Turning to me, Morty said, “These scoundrels are masters of Orwellian doublespeak,” and then he exited the call. About a year later, I chanced upon research that looks into actual word usage during earnings conference calls. Three authors, Paul Brockman, Xu Li, and S. McKay Price, examined transcripts from nearly three thousand such calls. One of the authors is interviewed […]

“Well Worth The Trouble”

How well positioned are you for the job market in a softening economic environment? Possessing the chartered financial analyst designation, known as the CFA charter, sends a strong signal to potential employers, said Chris Polson, President of the CFA Society Toronto, which is part of the global CFA Institute. He was speaking at the webinar “Capital Markets Compensation Trends” on August 11, 2015, sponsored by CFA Society Toronto. The goals of the webinar were twofold: to recap the value underlying the charterholder designation, and whether this was reflected in the remuneration of Canadian charterholders, as shown by the results of […]

Most Valuable Skill for Risk Managers?

In terms of marketable expertise for financial risk managers, what counts more: quantitative skills, or the ability to communicate and interpret the results of calculations? “The biggest surprise of our in-depth study is that communication ranked above quant skills,” said Christopher Donohue, Managing Director of Research and Educational Programs at the Global Association of Risk Professionals. On June 30, 2015, he reported on the results of the 2015 Job Task Analysis of GARP members. Survey Design The goal of the survey and analysis was to identify knowledge and skills necessary to support competent performance of tasks and responsibilities that are […]

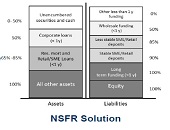

3 Steps to Liquidity Compliance

Are you scrambling to adjust to new reporting expectations for liquidity risk? Getting good data is key, but “you have to get it right and on time,” said Pierre Mesnard, Director Solutions Specialist at Moody’s Analytics. He was the third of three presenters on liquidity risk compliance at a webinar on June 25, 2015, sponsored by the Global Association of Risk Professionals. Once you have the data, there are three steps to delivering integrated liquidity compliance and business management, said Mesnard. First, you must ensure all financial instruments at your bank can be adequately modelled in order to generate realistic […]

Liquidity: A Change in Governance

Have you noticed that financial risk managers talk and think differently about liquidity risk, compared to pre-crisis days? The 2007-08 financial crisis was a watershed in the evolution of liquidity management, according to Nicolas Kunghehian, Director Solutions Specialist at Moody’s Analytics. He was the second of three presenters on liquidity risk compliance at a webinar on June 25, 2015, sponsored by the Global Association of Risk Professionals. “Before the crisis, there was only one team dedicated to monitoring and managing liquidity,” Kunghehian said. Liquidity risk was assumed to be small, and the Treasury department was chiefly fine-tuning the profit and […]

An Opportunity To Get Things Right

When it comes to forecasting liquidity risk, does your bank follow best practices? It might be tough to do so, because of a “data conundrum,” said Gudni Adalsteinsson, author of The Liquidity Risk Management Guide – from Policy to Pitfalls. Banks carry out a “retrospective analysis” on data that is “not forward looking.” Adalsteinsson, Head of Global Liquidity, Group Treasury at Legal & General Group Plc, was the first of three presenters on liquidity risk compliance, at a webinar on June 25, 2015, sponsored by the Global Association of Risk Professionals. He praised the Basel III regulation on liquidity risk. […]

Effective Risk Reporting

Effective risk reporting means “having the intelligence at your fingertips but exercising the judgment to report only what your company needs,” said Elizabeth Abraham, Director of Professional Services at MetricStream, and the second of two presenters at the June 16, 2015, webinar on Effective Risk Reporting sponsored by the Global Association of Risk Professionals. “Lack of clarity about the reporting objective” is a common barrier to effective enterprise risk management reporting, she said. Make sure you understand what level of information the audience wants. “Data model inconsistencies can lead to an inability to aggregate” the risk estimates, and that’s another […]

One Size Does Not Fit All

When it comes to risk reporting, do you ever feel that you are trying to push a square peg into a round hole? According to Gordon Goodman, that may happen rather often for companies that are not in the finance industry. Goodman, Director of Governance and Enterprise Risk Management at NRG Energy, was the first of two presenters at the June 16, 2015, webinar on Effective Risk Reporting sponsored by the Global Association of Risk Professionals. According to Goodman, there has been a push by banks to “bring their metrics to the marketplace, but this has created problems” for non-financial […]

Old Dog, New Tricks. List of Tricks

The following are a dozen helpful things I learned at a day-long seminar “The Power of Excel – Part 2,” held on location at the offices of the CFA Society of Toronto on June 10, 2015. The seminar was conducted by Jon Zelman of The Marquee Group. 1. Resist the Mouse 2. Best shortcut of the day 3. ALT-ernative Existence 4. If you filter, use SUBTOTAL, not SUM 5. To count the number of visible rows 6. Searching with multiple conditions 7. D is for Database function 8. “Exact” string matching versus “includes” 9. Multiple conditions for SUMIF 10. Weed out bad parameters early with Data Validation 11. Match and Index functions complement […]