Climate change is altering risk profiles the world over. In the US, it has led to an increase in wildfire season length, wildfire frequency, and the size of burned area. When it comes to such disasters, is the economic risk only borne by those in the risky area, or can the economic risk be shared among investors?

A recent webinar looked at a longstanding tool for financial adaptation. For nearly a century, mortgages have been used to create mortgage-backed securities (MBSs) in order to share the risk (and thus the return) of financing real estate.

“What are the benefits of securitization in an age where individual mortgage risk can be shared?” asked Amine Ouazad, Associate Professor at Rutgers Business School. On December 14, 2023, he presented his findings in a webinar, “Adaptation in Financial Markets: Climate Risk Pooling in Mortgage-Backed Securities” as part of the series of talks, the Virtual Seminar on Climate Economics, sponsored by the Federal Reserve Bank of San Francisco (FRBSF). His co-author was Matthew Kahn, Professor of Economics at University of Southern California Dornsife.

The researchers asked, is natural disaster risk exposure priced into MBSs over and above typical risk factors? Ouazad said there is a beta in finance that captures the correlations between cash flows and the wildfire risk factor, which is based on weather, climate, land cover, and infrastructure data.

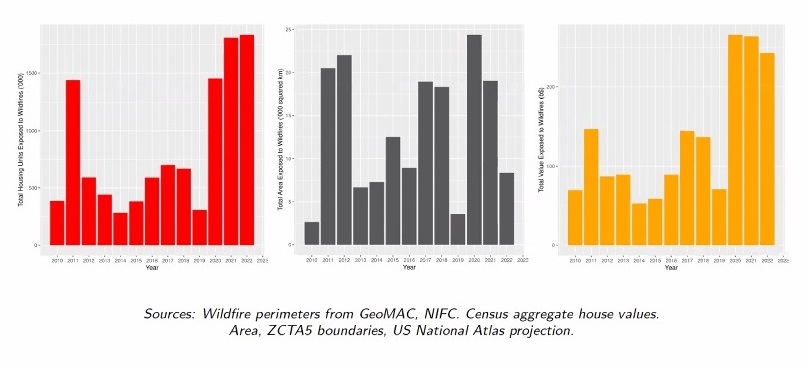

Using a national sample of private-label MBSs at monthly frequency, Ouazad found that wildfires led to “significant increases” in prepayments, defaults, and losses at the mortgage level. The losses can be measured in housing units, surface area of burn loss, or dollar value of loss. (Each of the three graphs shown here extend from 2010 to 2022.)

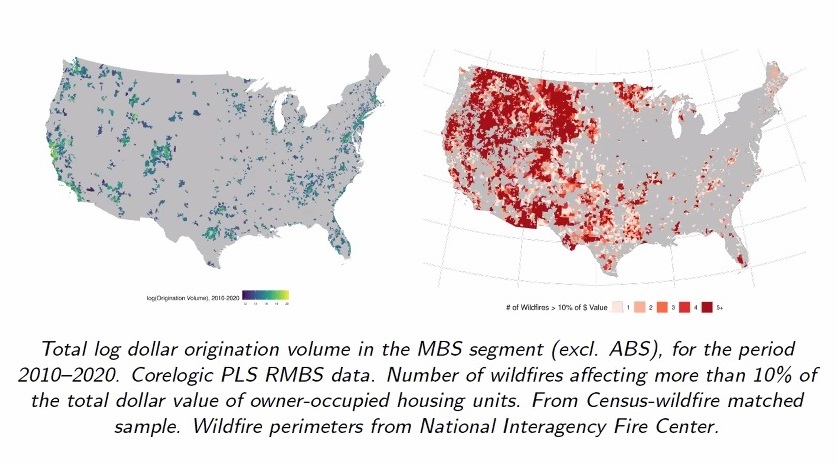

He showed two maps, contrasting locations of the mortgage originations of private-label securities (PLS) and locations of wildfires. The distributions are markedly different.

“At the deal level, wildfires caused significant increases in losses for undiversified MBSs,” Ouazad said, “but what is the impact for well-diversified pools?”

Ouazad asked, does wildfire risk affect cash flows when they are geographically diversified? He used two measures of spatial diversification in wildfire risk: “within-deal spatial correlation” and the Herfindahl index (HI) of the spatial concentration of dollar amounts. He found that risk depended on the “spatial correlation and the concentration of risk.”

He looked at three measures of climate risk diversification:

- Average MBS-level dollar-weighted wildfire propensity score.

- Spatial correlation of the dollar-weighted wildfire propensity score.

- The Herfindahl index of the distribution of dollar originations across ZIP codes.

Two of these measures involve the propensity score (PS), a tool to untangle complex data. The PS for a given individual area represents the probability of wildfire occurring, depending on having other, known, risky attributes. (For example, a forest area might have less sandy soil but be in a windier region.) Propensity score (PS) analysis is one of the most popular approaches for mitigating confounding effects.

The third measure, the Herfindahl Index, is a common measure of market concentration that is used to determine market competitiveness within a given industry sector.

“Wildfires have an economically and statistically significant impact on mortgage-level cash flows,” he concluded, “yet these effects are muted when deals are geographically diversified.” ♠️

Click here to see more of Professor Ouazad’s papers related to climate risk.

The wildfire pictures are from hotcore.info. Permission pending. The graphs are from the webinar presentation.

Click here to find out about the FRBSF Climate Seminar Series.