Greenhouse gases generated by human activities are contributing to the problem of climate change. For those who care about mitigating extreme weather and wildfires, the key global policy objective of this decade is to reduce carbon emissions.

One approach is the policy known as cap-and-trade, used by jurisdictions that create about 18 percent of global emissions. “Cap-and-trade” is shorthand for emissions trading, which is a market where regulators issue a limited number of emissions permits, and firms trade these permits among each other.

But lately the markets have been volatile. How well do cap-and-trade systems function when the global markets are in a state of high volatility?

“We begin with the hypothesis that carbon price uncertainty can delay investment decisions,” said Johannes Stroebel, who was presenting the webinar on October 16, 2025, as part of the Virtual Seminar on Climate Economics (VSCE) organized by the Europe-based Centre for Economic Policy Research (CEPR).

The talk was based on the paper “Carbon VIX: Carbon Price Uncertainty and Decarbonization Investments” by Maximilian Fuchs, Johannes Stroebel, and Julian Terstegge. Stroebel is Professor of Finance, New York University Stern School of Business whereas Fuchs and Terstegge are faculty at Copenhagen Business School.

Stroebel quoted anecdotal evidence from analyses of stakeholders. “Industry, business associations, commercial investors, and other stakeholders [state] that the carbon-pricing certainty gap is inhibiting investment.” He noted the effect of uncertainty is frequently mentioned but until now, has not been quantified.

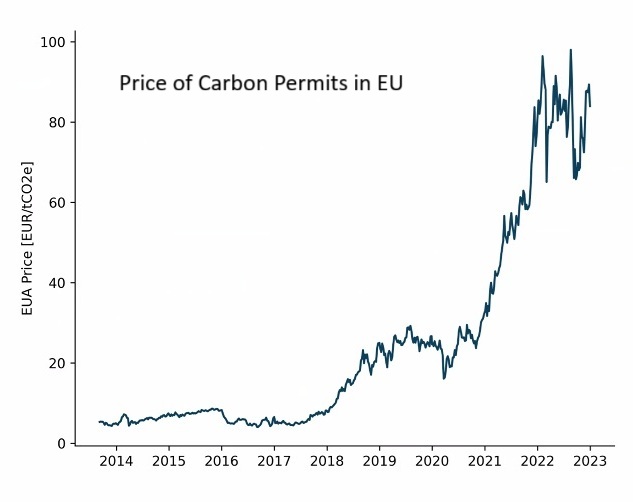

The researchers chose to study the EU Emissions Trading System (EU ETS), which is the world’s oldest cap-and-trade system, in place since 2005. A European Union Allowance (EUA) represents the permit to emit one tonne of carbon dioxide equivalent (CO2e). The markets for EUAs are well developed, consisting of primary (auctions), secondary, futures, and futures options. The graph below shows the price of permits over twenty years.

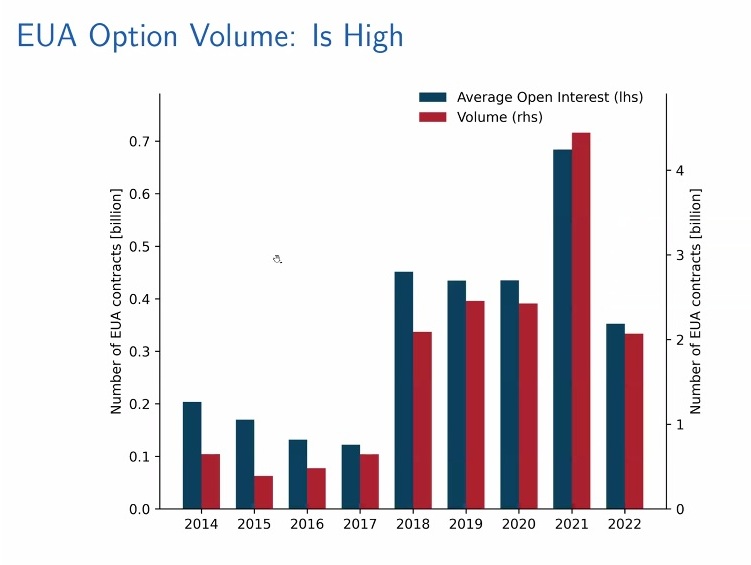

Furthermore, the option volume for permits is high.

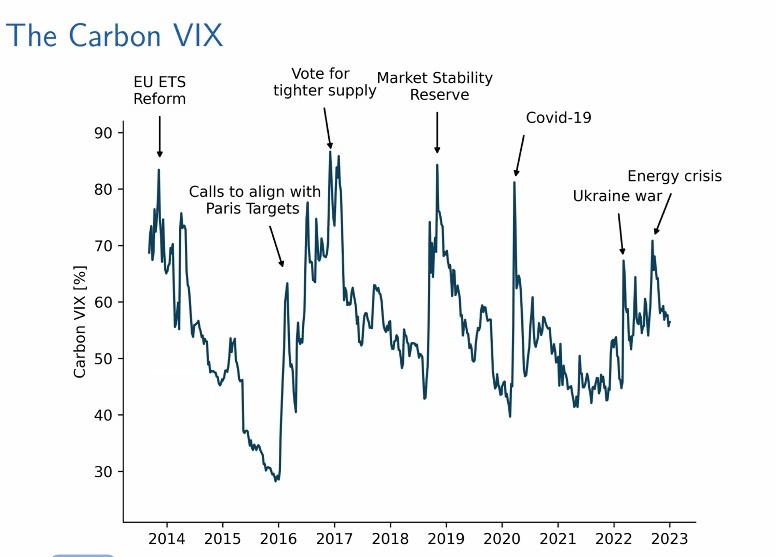

How to express volatility? The original VIX is the 30-day expected volatility of the SP500 index. Following the same methodology, Stroebel and co-workers constructed the “Carbon VIX,” “based on building a portfolio of options whose final payoff approximates the realized variance of EUA futures until option expiry.” He described it as a “model-free” treatment that requires liquidity across the moneyness.

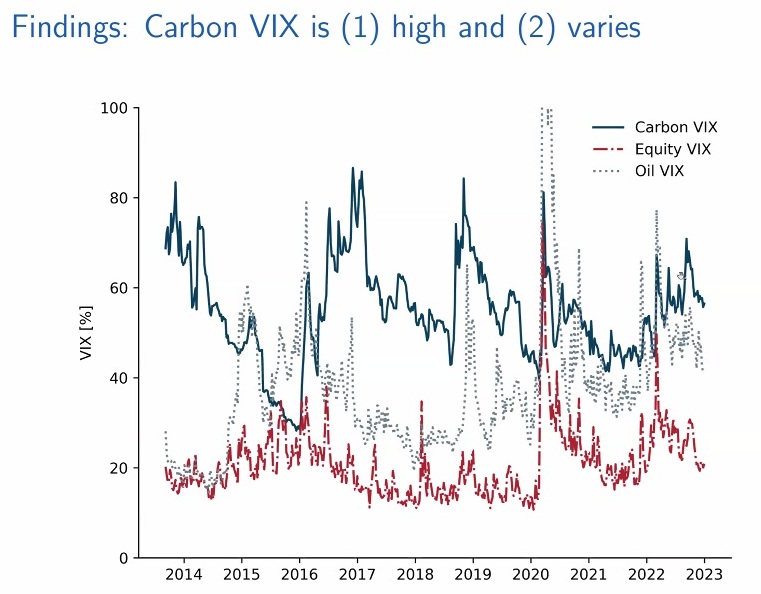

The VIX graph shows carbon price volatility varies substantially over time, with persistent shocks, as noted. It is high, currently with a VIX of 54 percent. Stroebel said, “Carbon VIX changes have moderate correlation with EUA price returns but low correlation with changes in equity and energy uncertainty. So it is a conceptually distinct uncertainty measure.” The graph below shows distinct patterns for three types of VIX: carbon (solid line), equity (dot-dash line) and oil (dotted line).

“When applied to emission trading systems, polluters have the real option to invest in decarbonization. However, if there is carbon price uncertainty, the value of delay will be greater than the value of exercising an option,” Stroebel said.

Next the question was, “Is there investment in decarbonization?” The researchers examined data from the Carbon Disclosure Project (CDP), based on 10,000 annual firm responses worldwide. Firms report emissions, emission targets, and abatement projects. The data are voluntary, not verified. For the abatement projects, they report activity type, amount invested, and give a textual description.

He showed a table of decarbonization investments by county. USA leads the way, both in terms of number of projects and the amount invested. In terms of industries, the utility and power sector is the most heavily invested in decarbonization, followed by manufacturing.

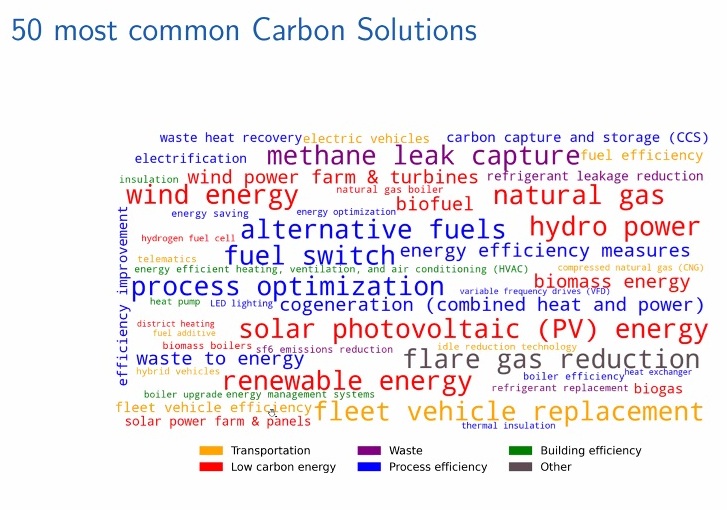

Stroebel and coworkers looked at the stock returns of the carbon solution providers. The chart below shows the top 50 text responses.

Stroebel and coworkers concluded that carbon price uncertainty is high and varies over time, with spikes around climate events. The uncertainty reduces investment in new technologies to decarbonize, and this has an aggregate effect. ♠️

Click here to view the VSCE webinar by Prof. Stroebel, “Carbon Pricing Uncertainty.”

Graphs are derived from webinar slides. Permission pending.

The thumbnail cartoon is from B. Rich Hedgeye. Permission pending.