Carbon Price Volatility

Greenhouse gases generated by human activities are contributing to the problem of climate change. For those who care about mitigating extreme weather and wildfires, the key global policy objective of this decade is to reduce carbon emissions. One approach is the policy known as cap-and-trade, used by jurisdictions that create about 18 percent of global emissions. “Cap-and-trade” is shorthand for emissions trading, which is a market where regulators issue a limited number of emissions permits, and firms trade these permits among each other. But lately the markets have been volatile. How well do cap-and-trade systems function when the global markets […]

The Future of Financial Advisors

How have investor expectations and behaviors evolved under the new U.S. administration? With recent strides in artificial intelligence, how is the role of the financial advisor changing? These and other questions were discussed by experts in behavioral finance during a webinar on April 16, 2025, titled “The Future of the Investment Professional: Mastering the Psychology of Investor Behavior.” The panelists touched on issues that will be discussed more fully at the upcoming conference, CFA Institute LIVE 2025 to be held in Chicago, 4-7 May, 2025. The panel moderator, Peter Lazaroff [Photo, RHS], is Chief Investment Officer at Plancorp Private Wealth […]

A Defining Moment

Investing in emerging markets amid today’s complex global landscape presents both opportunities and risks. Can investors identify markets with a strong potential for risk-adjusted returns? Can they avoid the worst of the pitfalls? In a webinar on March 19, 2025, three experts in the field presented a round-table discussion titled “Capital Flows, Tariffs & Trade: A Defining Moment for Emerging Markets Investors.” They touched on issues as wide-ranging as exchange rates, geopolitical risk, and trade barriers that will be discussed more fully at the upcoming conference, CFA Institute LIVE 2025 to be held in Chicago, 4-7 May, 2025. The panel […]

Transition & Stability

The increasing frequency of extreme weather events in Canada has caused the annual payouts for catastrophic insurance claims to skyrocket, according to a recent Statistics Canada report. This is but one small piece of a global picture emerging, where extreme weather events are causing homeowner insurance to increase at a rate higher than inflation. In the worst case, climate change will cause insurance companies to go bankrupt and homeowners will have nowhere to turn. “Transitions happen shock-wise and are systemic,” said Dirk Schoenmaker, Professor at the Rotterdam School of Management. “What can we do to reduce transition risk?” He was speaking at a webinar […]

Ask the Fed

“The Fed is trying to achieve price stability and maximum employment,” said Sylvain Leduc, Executive Vice President and Director of Research of the U.S. Federal Reserve Bank of San Francisco (FRBSF), known informally as “the Fed.” In terms of employment levels, he said, “We are back to where we were pre-pandemic.” He was speaking on February 7, 2023, at a public briefing in which he outlined the FRBSF’s thinking on economic matters. He showed a graph of unemployment, which reached a peak at the start of the pandemic in early 2020. The monthly change in nonfarm payroll employment had a downward […]

Chemistry and the Economy

Risks are multiplying and becoming more complex. The chemical industry is intrinsically connected to the economy. Can chemistry help solve the biggest crises facing us today? On December 15, 2022, the American Chemical Society hosted a virtual webinar, “Chemistry and the Economy.” The moderator was Bill Carroll, principal of Carroll Applied Science, who spoke to Paul Hodges, chairman of the Swiss-based strategy consulting firm New Normal. In speaking about risks, Hodges does not beat around the bush. He began with what he called “the four horsemen of the apocalypse.” He stated, “First there was the pandemic and associated supply chain […]

The Future of Crypto

What’s been happening in the cryptocurrencies market? Is it all merely speculation or is crypto here to stay? What is the future of broader blockchain technologies? What could regulation mean for the world of decentralized finance (DeFi)? On February 24, 2022, Helen Joyce, Britain editor of the weekly magazine the Economist, posed questions to her colleagues: Alice Fulwood, Wall Street correspondent at the Economist, and Matthieu Favas, finance editor at the Economist, in order to explore the rise of cryptocurrency and its potential consequences. “Blockchain can be thought of as a database distributed across many nodes,” Alice Fulwood said, “one […]

The future of active management

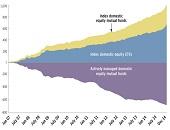

“Active portfolio management is futile,” say some who watch the progression of the financial industry. “Active managers only randomly outperform the stock market as a whole.” Is this true, or have the rumours of its demise been greatly exaggerated? On June 10, 2021, Philip Young, CFA, welcomed a webinar audience on behalf of the CFA Society of Toronto to consider this very question as they listened to Ronald Kahn, Managing Director, and Global Head of Systematic Equity Research at Blackrock, the world’s largest asset manager. He recently co-authored the book Advances in Active Portfolio Management: New Developments in Quantitative Investing. […]

Death of Fundamental Analysis?

Have you been following the market frenzy around stocks for GameStop, AMC and Bed Bath & Beyond? Or the news on Wall Street Bets and Robinhood? How disruptive are these events for traditional valuation methods? What new factors must be considered when investing and allocating capital? Recent shifts in market dynamics have altered the perception of capital markets in meaningful ways. On April 8, 2021, the Corporate Finance Committee of the CFA Society of Toronto convened a panel of experts to discuss the reasons market valuations are so out of synch with fundamental analysis. Moderator Stephen Foerster, Professor of Finance […]

“Disasters Everywhere”

What is the cost of a disaster? What is the cost of the business cycle? Economically speaking, how do business cycles compare with disasters? The cost of business cycles and the gain to be had from stabilization policy is a highly controversial topic in macroeconomics. Some believe the welfare gains from stabilizing the business cycle are extremely low and therefore not worth the effort. “Depression prevention and stabilization policies are central to the discipline of macroeconomics,” conclude the authors of recent research published by the Federal Reserve Bank of San Francisco. “Extreme and costly events are not the only reason […]