“The inter-connectedness of the regulatory landscape has increased dramatically,” said Balachander Lakshmanan, Director at Deloitte & Touche LLP. He was the first of two presenters at the June 24, 2014, webinar sponsored by the Global Association of Risk Professionals to discuss the impact of capital rules on risk rating systems.

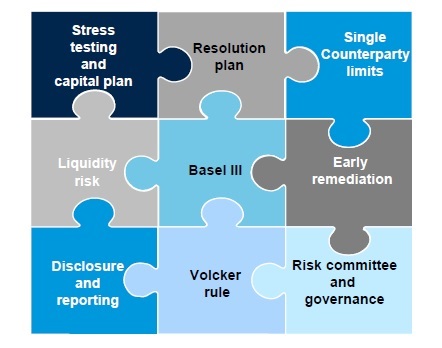

In the wake of the financial crisis, new regulations—Basel, Volcker rule, Comprehensive Capital Analysis and Review (CCAR)—have proliferated. Due to changes in capital rules, new operating models are starting to emerge at banks, said Lakshmanan. There are requests for “spot calculations” or snapshots of a bank at any given time. There are requests for future projections, including financially stressed futures. As well, new regulations around governance require proof of effective controls and independent review.

The lowest common denominator of all requests? According to Lakshmanan, it is the financial models themselves. Models are critical for regulatory compliance. For example, “a Basel requirement is that each debtor must be rated at least once.”

Activities with respect to models fall into three types: development, implementation, and independent model review. Banks need to ensure the three “factories” of these activities work seamlessly with each other.

For the remainder of his presentation, Lakshmanan chose to focus on model implementation so he could explore the challenges or “the big choke points.”

“Models must be made available to a diverse user base,” for example, to underwriters, and to those who report on overall risk management. Different users prefer different platforms, with some using the model “like a calculator,” he said.

“Some complex models are only available in spreadsheets,” said Lakshmanan, and this fragmented technology, as well as constant changes to the portfolio, presents a challenge to implementation of a robust risk ratings system.

Lakshmanan emphasized that “clear governance and processes around data supporting the models is critical.” An area of regulatory focus is how “nimble” the system can be: whether data from the field can be sourced, cleaned and prepared for use in models. Users and regulators expect an efficient turnaround for data preparation.

“Risk ratings should not just serve origination but also help in other functions, such as assessing economic capital,” said Lakshmanan. Challenge models—those designed to be run side by side with accepted models—are also required.

Lakshmanan closed his presentation with a summary of best practices and key challenges for the IT implementation of models. We quote his list of key challenges here:

1) Lack of common identifiers and reference database

2) Numerous credit applications and risk rating systems

3) Lack of quality data, or aspects of required data not captured

4) Benchmarking with external rating agencies not available

5) Inadequate training of bank personnel

6) Different risk rating scales / granularity

7) Risk-focused supervision and increased concern with ongoing monitoring / validation

These will serve as a to-do list for those who are improving risk rating systems world-wide. ª

Click here to read about the second presentation, a case study of risk ratings. ª

Click here to view the webinar presentation on impact of capital rules on risk ratings. Lakshmanan’s portion is slides 4-12, with the key challenges summarized on slide 12.

The graphic featured in this posting was modified from slide 6.