Integrated Data and Modelling

How can today’s bankers prepare for tomorrow’s challenges? Consider the financial models built using available data. Data collection and financial modelling used to be conducted in each different silos of the bank, with credit separate from market, which was separate from treasury and other groups). Then data became “managed” and modelling was moved to “platforms” which did not mix well between the various silos. A few brave souls began to integrate the data management for different groups of the bank. Other brave souls tried to integrate the modelling. This was the phase of integration achieved through batch calculations. Now, the […]

The Latest & Greatest

Although the next round of changes to accounting standards will not come into effect until 2018, alert financial analysts should already be asking companies about how they plan to address them, according to Canada’s top accountant. “Pay attention now, because companies do have the option to adopt” and some, such as Canadian banks, are adopting IFRS 9 early, said Linda Mezon, Chair of the Accounting Standards Board (AcSB). She was speaking at a webinar on January 21, 2016, to members of CFA Society Toronto and CPA Canada on the recent developments in accounting standards and emerging trends impacting financial statements. […]

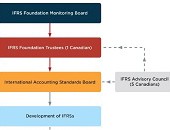

“Feedback Difficult to Obtain”

In the financial world, change is a constant. Regulators can barely keep up. Who decides what regulatory changes need to be made? And who can apply the brakes, if a certain type of change is having unintended consequences? Canada’s top accountant briefed the members of the CFA Society Toronto jointly with CPA Canada at a webinar on January 21, 2016. “Feedback is important but difficult to obtain,” said Linda Mezon, FCPA, FCA, who is the Chair of the Accounting Standards Board (AcSB). She summarized how Canadians and the AcSB influence the development of International Financial Reporting Standards. “The Accounting Standards […]

Three-Way Damage

Do you remember that cute VW video, “The Force”? The one where the little boy, dressed up as Darth Vader, can’t get a reaction from anyone or anything, even his dog, when he tries his super-powers on them? Then, Dad drives up in his VW Passat and the Vader-wannabe is, magically, able to get the lights to flash. The camera pans to parents looking out the window. Dad gives a conspiratorial grin as he clicks the remote control. On September 18, 2015, world markets were rocked by news that Volkswagen had knowingly falsified its emissions of toxic nitrogen oxides. The […]

Currency Option Trading Strategies

Throughout 2015 currency volatility has been increasing, even among established currencies such as the Swiss franc. Persistent exchange rate volatility can be an especially serious problem for currencies of emerging economies. Central banks often intervene by using foreign exchange reserves to purchase and sell foreign currency directly in the spot market. This relies on the continuous accumulation of foreign exchange reserves, which may be very difficult for emerging economies. How, then, can the central banks of such nations best manage currency fluctuations? In 2007-8, when the Colombian peso exchange rate was volatile, the Colombian central bank tried various strategies in […]

Watch Out for Hippos

Is your company managing risk well enough to make the most of opportunities as they appear? Or does it suffer from risk paralysis? As a company matures, it moves from trying to identify all possible risks (and mitigating them), to saying “what risks will give me the chance to pursue an opportunity,” said Martin Pergler, Founder and Principal of Balanced Risk Strategies, Ltd. He was the first of two panellists at the webinar titled Explore Your Opportunity Landscape by Harnessing Your Risks, sponsored by the Global Association of Risk Professionals on November 18, 2015. Pergler began by making a memorable […]

Harnessing Your Risks

Before your company undertakes economic risks, what systems should be firmly in place? “Good risk management allows us to take risks we wouldn’t normally do,” said Brenda Boultwood , Senior Vice President of GRC Solutions at MetricStream. (GRC is the acronym for governance, risk management and compliance.) She was the second of two panellists at the webinar titled Explore Your Opportunity Landscape by Harnessing Your Risks, sponsored by the Global Association of Risk Professionals on November 18, 2015. A company needs superior risk intelligence in order to understand the risks they plan to harness. Technology can be leveraged to capitalize […]

Topology Can Streamline Modelling

How can software systematize and optimize the routine tasks in building financial risk models? “We use topology to inform feature selection, and then we examine a range of models,” said Mukund Ramachandran, Data Scientist at Ayasdi. He was the third of three panellists at the October 27, 2015, webinar on Effective Risk Models Using Machine Intelligence sponsored by the Global Association of Risk Professionals. In the course of evaluating potential models, several statistical tests are applied. “Machine intelligence considers the entire high dimensional space jointly,” he said. Machine learning is capable of applying hundreds of algorithms and different combinations, “but […]

Machine Intelligence + Business Intuition

Given the exponential growth in data complexity, how can you, the risk manager, quickly determine the most salient economic factors to include in calculating a bank’s risk exposure? Nowadays, modelling risk is all about “speed, accuracy, and defensibility,” said Patrick Rogers, Head of Marketing at the software company Ayasdi. Risk models must be developed “in a relatively short time window and must be statistically valid.” Since risk models must be defensible to business owners and industry regulators, and simple to explain, the ordinary “black box” machine learning would fall flat, Rogers said. He was the second of three panellists at […]

“Tons of Models, Tons of Variables”

With so many economic variables, and such a wide choice of parameters, do you feel overwhelmed by the task of producing the best financial model possible? Is there a systematic approach to exploring models? “Ever since the 2008 financial crisis, there’s been a focus on stress testing,” which requires robust financial models, said Roderick Powell, Director of Market and Treasury Risk at the consulting company KPMG. He was the first of three panellists at the October 27, 2015, webinar on Effective Risk Models Using Machine Intelligence sponsored by the Global Association of Risk Professionals. “Building those models is a time-consuming, […]