Throughout 2015 currency volatility has been increasing, even among established currencies such as the Swiss franc. Persistent exchange rate volatility can be an especially serious problem for currencies of emerging economies.

Central banks often intervene by using foreign exchange reserves to purchase and sell foreign currency directly in the spot market. This relies on the continuous accumulation of foreign exchange reserves, which may be very difficult for emerging economies.

How, then, can the central banks of such nations best manage currency fluctuations?

In 2007-8, when the Colombian peso exchange rate was volatile, the Colombian central bank tried various strategies in the currency markets to influence the direction of the exchange rate, said Helena Keefe, Professor of Economics at Fairfield University. She was speaking at the December 10, 2015, Global Association of Risk Professionals webinar on currency option trading strategies.

First, Keefe presented a brief synopsis of the Colombian peso movements during the period 2007-2008. In collaboration with Erick Rengifo , Professor of Economics at Fordham University, she built a Matlab model to simulate a central bank trying to manage a depreciating Colombian peso using currency options (and later, an appreciating peso).

The lessons learned from Colombia showed volatility options were successful in smoothing currency fluctuations. Currency options will avoid excessive reserve accumulation, while increasing liquidity and building markets, the researchers noted.

{kind=link}

“Volatility put options were auctioned during periods of appreciation,” said Keefe, “and volatility call options were auctioned during periods of depreciation.” The options were exercised on any day when volatility exceeded a pre-specified amount—even the auction date. She monitored the difference from the moving average as a function of time for 2, 5, and 10 days after the event.

“Trend reversion occurred in 90 percent of the cases,” Keefe said. Visual inspection of the moving averages showed the strategy was effective in nearly every case, except for two dates that had significant other politico-economic occurrences.

“We can conclude that exercise of options did lower the volatility—which was the goal of the central bank,” she said.

However, the central bank did not continue the program. Keefe said they had found distinct evidence supporting the central bank’s actions. She called the abandonment of currency options by the central bank of Colombia “premature.”

The near-success of this real-life case spurred the researchers on to develop a more robust currency option for use by central banks: the W-strategy for intervention.

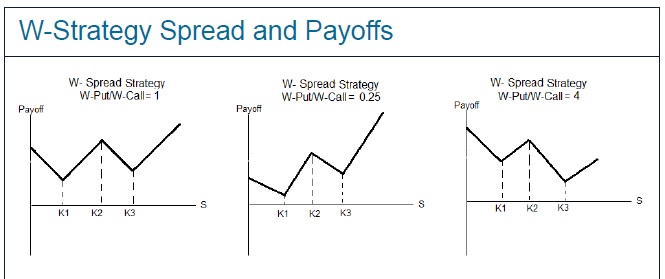

The W-strategy involves combining a W-call and a W-put. (See figure below.) “The central bank can hold more puts, or more calls, depending on their strategy of appreciation or depreciation,” Keefe said. “Here, we focus on a neutral strategy.”

They priced options using the Garman-Kohlhagen model, determined delta for daily hedging activity, and then analyzed the spot market position of central bank. From that they calculated costs, transaction value, payoffs and premiums.

Overall, they found the W-strategy, using currency options, enabled the central bank to manage volatility. There are other benefits, too, of the W-strategy, such as increased liquidity by creating more trading positions.

They plan to do further research in the area of emerging economies. They emphasized one important caveat in their model: “the W strategy only works properly when the market fundamentals are in place. If the economy of the nation is undergoing upheaval—for example, if there is a fundamental shift from an export-based economy to a consumer-based economy, the model might not work well. ª

Click here to view the webinar presentation.

The research paper it’s based on can be found at: http://isiarticles.com/bundles/Article/pre/pdf/40304.pdf

The image of Colombian currency is from mypivots.com

The image of the Colombian market is from Tripadvisor.com