The Fed, Foreign Banks and Basel III: Part 1. A Long Hard Look

Foreign banking operations (FBOs) in the United States are about to face a whole new set of regulations that may dampen their enthusiasm for US-based operations, according to a February 14, 2013 webinar organized by the Global Association of Risk Professionals (GARP). “The Fed observed over time that US branches were increasingly used to fund the home office operations,” said Charles Horn, partner at Morrison Foerster, who was the first speaker at the panel. Other concerns of the Federal Reserve Board are the increased complexity of FBOs, and “the availability of home country financial resources for branch offices.” The goal, […]

Managing Model Risk: Part 2. The Impact of Basel III

“More consideration must be made for regulatory capital changes that focus on small but potentially devastating risks or risk factors,” said Peter Went, VP, Banking Risk Management Programs at GARP. He was speaking about Basel III and its impact on modelling regulatory capital at a webinar on January 29, 2013, organized by the Global Association of Risk Professionals to discuss model risk management. Went mentioned three developments in the Basel III that directly impact capital models and model risk in regulatory capital determination. First, Basel III introduces a risk-invariant leverage ratio of 3 percent in recognition that models may be […]

Basel III Burden: Part 3. “Our Business Achieved Tangible Benefits”

The third and final speaker at the October 18, 2012 GARP webinar on the Basel III burden on profitability was Alyson Bailey-Flynn, Director in Global Analytics and Financial Engineering at Scotiabank. She had a good news story to share. “Improved risk management meant improved decision-making,” she said, prior to delivering a brief survey of the implementation of risk management at Scotiabank. When it came to market risk calculations, management was both for and against spreadsheet usage. (“For” because it meant ease of use; “against” because it meant lack of control.) Ultimately Scotiabank chose an in-house batch risk engine powered by Algorithmics Risk […]

Basel III Burden. Part 2: The Devil is in the Data

The second speaker at the October 18, 2012 GARP webinar was Peyman Mestchian, Managing Partner, Chartis Research. The Basel III “journey” will have three main impacts in financial institutions, he said: (1) Improved capital management. Mestchian believes banks will figure out how to adapt “without sacrificing their efficiency”; (2) Greater integration of risk, compliance, and finance functions. There will be overlapping responsibilities for Basel III, between front office, finance & treasury, and risk & compliance departments; and (3) Implementation of enterprise-wide risk management systems. Under Basel III, “capital optimization has a much higher profile,” Mestchian said. “Due to short timelines, […]

Basel III Burden: Part 1. From Too-Big-To-Fail To Too-Small-To-Survive

Basel III regulations are onerous and complex, but must ultimately be managed, according to a panel of three banking experts who made presentations during the October 18, 2012 Global Association of Risk Professionals (GARP) webinar to an audience estimated at around a thousand. The webinar follows on the heels of a McKinsey report that estimates banks’ average return on equity (ROE) will drop from 20 percent ROE in 2010 to 7 percent upon Basel III implementation. The session was kicked off by Mario Onorato, Senior Director, Balance Sheet and Capital Management, IBM, who talked about business models and IT implications. […]

Impact of Basel III on Capital Instruments. Part 2: Football vs. Soccer

On August 16, 2012, speaking at a webinar hosted by the Global Association of Risk Professionals (GARP), three panellists gave a perspective on the changes Basel III would wreak on capital instruments. Click here for Part 1. The second speaker, April Frazer, Director of Client Solutions Group at Wells Fargo, gave an overview of the impact of the US Basel III proposal on market dynamics. Due to regulatory limitations that she is subject to as a member of a financial institution, her talk is not reported on here. Steve Sahara, Global Head of DCM Solutions and Hybrid Capital, Crédit Agricole […]

Impact of Basel III on Capital Instruments. Part 1: Ramp-up in Capital

On August 16, 2012, three panellists gave a perspective on the changes Basel III would wreak on capital instruments. It was a highly detailed talk, delivered at high speed, with many qualifications made to the main points, but the sponsoring organization GARP has done a tremendous service to its membership by gathering together these experts. There are some excellent summary slides (link below). This two-part posting showcases the top messages from the three experts, Dwight Smith, April Frazer, and Steve Sahara. In June 2012, three US regulatory bodies (the OCC, the Federal Reserve Board, and the FDIC) proposed three sets of […]

US Implementation of Basel III. Part 2: The GPS for the Journey

On July 24, 2012, Peter Went, VP Banking Risk Management Programs at GARP, summarized the changing landscape of Basel III from a US perspective. First he outlined the deadlines and proposed changes; Part 1 of this posting covers these for the standardized approach. Financial institutions adhering to the advanced approach, Went said, must follow the Basel III counterparty credit risk rules. In some cases, correlations between asset values must be increased. A distinction will be made between securitization and resecuritization. [Ed. Note: To this, we say, “high time.” See, for example, Hull & White’s award-winning article in Financial Analysts Journal, […]

US Implementation of Basel III. Part 1: A Long and Winding Journey

The long and winding US route to Basel implementation has been more difficult and circuitous than the route for European banks. Peter Went, VP Banking Risk Management Programs at GARP, delivered a webinar update on the Basel III leg of the journey on July 24, 2012. First, Went summarized the deadlines. Several sequential proposals have been issued by the US prudential agencies: the OCC, FRB, and the FDIC, with an expected implementation date beginning January 1, 2013, and a series of milestones thereafter. [Note: by mid-December 2012, the implementation dates for most of the Basel III proposals have been delayed […]

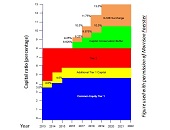

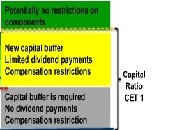

Risk-Based Capital Requirements under Basel III: Part 2. The More Capital, the More Stability

On July 17, 2012 Peter Went, VP Banking Risk Management Program at the Global Association of Risk Professionals (GARP), addressed a webinar audience on the significant changes to capital requirements under the new Basel III rules, as was reported in the Part 1 posting. According to the survey of the Basel Committee Basel III Monitoring Exercise, many banks have embarked on aggressive campaigns to raise capital. In addition to increasing existing capital requirements, Basel III proposes two new charges: the capital conservation buffer, which may require banks to maintain an additional 2.5 percent, and the countercyclical buffer (shown in the […]