Swaps, Before & After

“Historically, there were few, if any, regulatory requirements on swaps … it was effectively an unsecured loan,” said James Schwartz, Of Counsel at Morrison & Foerster. He was the fourth and final presenter at the Derivatives Regulatory Update webinar held on March 31, 2015, sponsored by the Global Association of Risk Professionals. Prior to the Dodd-Frank Act, swaps dealers were self-regulated through the trade association International Swaps and Derivatives Association (ISDA). “It was typical for the two parties to accept a certain amount of uncollateralized exposure to each other in the form of a threshold that varied according to their […]

Update on Central Clearing

One of the goals of the Dodd-Frank Act is to mitigate systemic financial risk by establishing a central clearinghouse for derivatives. But how close is the financial community toward achieving that goal? “Many swaps were not collateralized prior to Dodd-Frank,” said Julian E. Hammar, Of Counsel at Morrison & Foerster. Hammar was the third of four presenters at the Derivatives Regulatory Update webinar held on March 31, 2015, sponsored by the Global Association of Risk Professionals. Clearing swaps mitigates risk not just through requiring margin collateral (and thereby reducing) credit risk. It also imposes an “operational discipline” Hammar said, with […]

“Skin in the Game”

What safeguards should be in place, to minimize the risks posed by financial derivatives? CME Group requires that its Clearing Members support the risk of their portfolios by “putting some skin in the game,” said Jason Silverstein, Executive Director and Associate General Counsel of CME Group, a body that includes the Chicago Mercantile Exchange and the New York Mercantile Exchange among its subsidiaries. “It’s a story of balancing incentives, in order to stabilize losses. Our belief is that it should be significant and risk-based.” Silverstein was the second of four presenters at a webinar titled Derivatives Regulatory Update held on […]

Towards Reducing Systemic Risk

Have the risks posed by financial derivatives in the context of the current, still evolving, regulatory landscape been properly addressed? Michael Piracci, Director of PCB Compliance at Barclays, said that nowadays he has “a lot of interactions day-to-day with the clearinghouse” and overall, “it makes me feel a little more comfortable there’s a good system in place.” Piracci was the first of four presenters at a webinar titled Derivatives Regulatory Update held on March 31, 2015, sponsored by the Global Association of Risk Professionals. Piracci began by explaining the role of the Central Counterparty (CCP) and the Futures Commission Merchants […]

Tailoring Risk Model to Investment Strategy

Due to the growing complexity of measuring financial risk, “risk has become a patchwork” of different models, said Phil Jacob, Senior Director at Axioma Risk Research. He was the sole presenter in a webinar about tailoring the right risk model to your investment strategy held on March 4, 2015, and sponsored by the Global Association of Risk Professionals (GARP). Jacob identified four inherent challenges. “There are operational issues stemming from existing rigid approaches,” leading to “difficulty in aggregating risk.” There is a lack of consistency in modeling portfolios, which can run the gamut from very simple proxies all the way […]

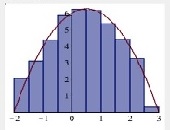

Clickable Calculus

When finding a definite integral, do you spend an inordinate amount of time in the step-by-step algebra? Let’s say you are integrating over a probability of default function that has been fitted to real-life data (a non-normal curve) and you want to understand step-size dependence. Or perhaps you are a beginning student of mathematical finance, reviewing the fundamentals of integration, and you just wish there was a faster way to change functions and spit out a graph. “Integration is a summative process, and the applications that show this can become a time-sink,” said Robert Lopez, Emeritus Professor of Mathematics at […]

Investing in Emotional Assets

When Morty discovered my vacation plans this year included Cremona, that put a bee in his bonnet. Did I know it was the home of the famous Stradivarius workshop? Was I going there to check out violins? Yes and no, I said. My preference was to cycle along the Po valley and sip espresso near the Zodiac Tower. “Maybe you should think twice about your visit,” Morty said. “I happen to have it on good authority that beautiful collectibles can be a solid component of your portfolio.” “Please Morty, don’t make wild-eyed guesses about other people’s money,” I said. Especially […]

Interview with William Bernstein: The Paradox of Wealth

I could hear the laughter from down the hall. “Cheeseburger,” cried Morty. Cheeseburger? I saw he was holding a back issue of the Financial Analysts Journal. (It’s no secret that we fall behind on our reading here during the busy months.) “You’ve gotta interview this guy,” declared Morty. “Anyone who can work the word ‘cheeseburger’ into the pages of this esteemed journal… well… he likely has something interesting to say.” William Bernstein did indeed have some very interesting things to say. The interview below is the vegan-friendly edition, though; if you want to see ‘cheeseburger’ in print you’ll have to […]

Fama-French 2. Three is Now Five?

Fama and French, originators of the three-factor model for asset pricing, are working to understand the fourth factor –and a fifth factor, too, said Marlena Lee, PhD, VP of Dimensional Fund Advisors. She should know; she has worked closely with Nobel laureate Gene Fama and was his former teaching assistant at the University of Chicago Booth School of Business. Lee spoke at the CFA Society Toronto on June 19, 2014, about the evolution of asset pricing. Part 1 summarizes her comments on the dimension of profitability. Could there be another component? As early as 1993 Jegadeesh and Titman had proposed […]

Fama-French Model 1. Three is Now Four

Does the Fama-French three-factor model adequately capture all information available in describing stock returns? According to Marlena Lee, PhD, VP of Dimensional Fund Advisors, the three-factor model is lacking one or two important components. Lee visited the Toronto offices of the CFA Society Toronto on the afternoon of June 19, 2014, to speak to over twenty financial experts about the evolution of asset pricing. Lee was a funny and forthcoming lecturer. After her flight from the States up to Toronto, she said the suspicious Canada Border Services officer asked: “This CFA Society… what does ‘CFA’ stand for?” She momentarily blanked: […]