The Fed, Foreign Banks and Basel III: Part 2. Capital Concerns

“Some of the rules are in direct conflict,” said Peter Went, VP, Banking Risk Management Programs, GARP. He was the second speaker at a webinar presented on February 14, 2013 organized by the Global Association of Risk Professionals (GARP) regarding regulatory reform of foreign banking operations (FBOs) in the United States and the implementation of the Basel III framework. The “conflict” refers to rules in the Dodd-Frank Act versus the globally agreed Basel III Accord’s guidelines. Both regulatory attempts apply the G-20 principles on financial regulation (Pittsburgh 2009 summit). The US implementation of the Basel III framework differs from the […]

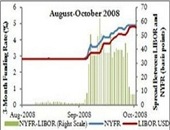

Libor Fallout: Part 2. Whistling Past the Graveyard

On December 20, 2012, the second presenter at the GARP webinar on the LIBOR scandal was Cliff Rossi, Executive-in-Residence, Center for Financial Policy, University of Maryland. He described the risk implications arising from the Wheatley Review of LIBOR. Rossi noted that some market participants were “still feeling PTSD from the financial crisis of 2008”—and then they got hit with the LIBOR scandal. Rossi succinctly described what went wrong: Low volume in interbank lending in unsecured transactions created an over-reliance on “expert judgement” hence the rate was subject to manipulation. Part of the problem, Rossi said, is that LIBOR reporting was […]

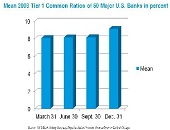

Contingent Capital: The Case for COERCs. Part 1

Contingent convertible bonds, or “cocobonds,” are bonds that convert into equity when the market value of capital falls below a trigger level. A major problem with cocobonds is that “the conversion trigger is based on the capital ratio, which is known to be a poor indicator of financial distress,” said Theo Vermaelen, Professor of Finance at INSEAD. He was the first speaker at the November 29, 2012 webinar held by the Global Association of Risk Professionals (GARP) on the subject of Call Option Enhanced Reverse Convertible (COERC) bonds. Vermaelen referred to a case in point: a Credit Suisse cocobond issued […]

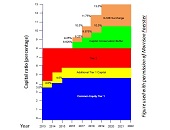

Impact of Basel III on Capital Instruments. Part 1: Ramp-up in Capital

On August 16, 2012, three panellists gave a perspective on the changes Basel III would wreak on capital instruments. It was a highly detailed talk, delivered at high speed, with many qualifications made to the main points, but the sponsoring organization GARP has done a tremendous service to its membership by gathering together these experts. There are some excellent summary slides (link below). This two-part posting showcases the top messages from the three experts, Dwight Smith, April Frazer, and Steve Sahara. In June 2012, three US regulatory bodies (the OCC, the Federal Reserve Board, and the FDIC) proposed three sets of […]

Reality vs Expectations: What Risk Managers Can Learn from the NFL

Arriving a little late at the CFA Society Toronto luncheon on June 4, 2012 at the National Club on Bay Street, I had a lucky choice of seat at the “hodge podge” table near the back. My two nearest neighbours at the table had driven from Simcoe to Toronto that morning (a minimum two-hour trip) for the express purpose of meeting the featured speaker, Roger Martin, Dean of Rotman School of Management. One said he had not only read and enjoyed Martin’s latest book, Fixing the Game: Bubbles, Crashes, and What Capitalism Can Learn from the NFL, he had also […]

“We Need to Fix the Plumbing”

Allan Grody is a man with a mission. The fall-out from the financial meltdown has shone a light on many things that need fixing within the financial system, and of these, Grody is focusing on one especially leaky, corroded pipe. Grody, president of Financial Intergroup, was addressing a GARP (Global Association of Risk Professionals) audience as the third of three panelists on “Modernizing Financial Risk Management: The Changing Technology Paradigm” on May 22, 2012. Early in his presentation, Grody showed a complex summation diagram. Titled “Need to Fix the Plumbing,” it was a kind of map, one that deserves a place […]

Real-Time Risk Analytics, SAS Style

“Analysts in capital markets get pummeled with vast quantities of information,” said Jeff Hasmann, “sometimes receiving as many as twenty newsfeeds per day. How are they to make sense of it all?” Hasmann was the first of three panelists speaking at the Global Association of Risk Professionals (GARP) webinar, “Modernizing Financial Risk Management: The Changing Technology Paradigm” on May 22, 2012. There is a push to modernize financial risk management from both above and below. Besides handling information overload, Hasmann noted there are several reasons to modernize: evolving regulations, improvements in efficiency to be gained, and needs for standardization. Hasmann, […]

Joost Driessen Discusses Liquidity Effects in Bonds

Put away the crossword and the sudoku: it’s the “credit spread puzzle” that’s occupying some leading financial minds. On May 3, 2012, Prof. Joost Driessen of Tilburg University spoke to a Global Association of Risk Professionals (GARP) webinar audience about recent work done by his research group to solve this puzzle. The term “credit spread puzzle” refers to the fact that credit spreads are much higher than can be justified by historical default losses. A typical example Driessen cited was a long-term AA bond that had an expected default loss of 0.06% yet whose average credit spread, calculated using real-life data, was 1.18%. More […]