Platform of the Future

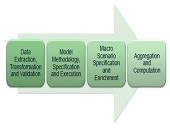

What will be the ideal modelling platform of future bankers? It will need to contain key functionalities in model execution, scenario management, and a “risk engine” that will deliver answers for multiple horizons at the loan level. Furthermore, it should implement the most advanced modelling suites, reduce the quants’ time to develop models, and contain simulation capabilities for stress testing and beyond. This bold vision of the future was presented by Martim Rocha, Advisory Business Solution Manager at SAS. He was the second of two presenters at the February 25, 2016, webinar offered by the Global Association of Risk Professionals […]

“Tons of Models, Tons of Variables”

With so many economic variables, and such a wide choice of parameters, do you feel overwhelmed by the task of producing the best financial model possible? Is there a systematic approach to exploring models? “Ever since the 2008 financial crisis, there’s been a focus on stress testing,” which requires robust financial models, said Roderick Powell, Director of Market and Treasury Risk at the consulting company KPMG. He was the first of three panellists at the October 27, 2015, webinar on Effective Risk Models Using Machine Intelligence sponsored by the Global Association of Risk Professionals. “Building those models is a time-consuming, […]

Lagging in Technology Solutions

When it comes to new regulatory requirements for advanced models in financial stress testing, are banks meeting expectations? Over the past two years, relatively good progress has been made in financial models and managing data for stress testing, said Tom Kimner, Director of Global Risk Operations at SAS, “but less progress has been made in technology and reporting.” He was the second of two panellists at a webinar on September 22, 2015, sponsored by the Global Association of Risk Professionals (GARP). He was presenting the findings from a survey report, “Stress Testing: A View from the Trenches,” that was jointly […]

Rising to the Challenge

What kinds of financial institutions are scrambling to comply with new regulatory requirements for financial stress testing? In 2015, the Global Association of Risk Professionals (GARP) conducted its first industry survey to see how banking institutions worldwide were coping with more stringent regulations. They produced a report, “Stress Testing: A View from the Trenches,” and on September 22, 2015, two panellists presented their findings during a webinar to members of GARP. “Institutions on the whole are purposefully addressing the challenges,” said Jeff Kutler, Editor-in-Chief of Risk Intelligence at GARP. “There has been significant progress in data, modeling, and scenario management.” […]

Four Lessons from Stress Testing Exercise

“It very quickly became apparent that this was not a one- or two-month exercise,” said Charyn Faenza, Vice President, Manager of Corporate Business Intelligence Systems at First National Bank, the largest subsidiary of the largest subsidiary of FNB Corporation. She was the second of two presenters at the May 19, 2015, webinar on Stress Testing Modeling sponsored by the Global Association of Risk Professionals. Faenza was referring to her bank’s experience as an example of a “DFAST 10-50” bank that is required to conduct an annual stress test. She drew four important lessons from the exercise. Good Modeling Requires Good […]

“Not Only The What But The How”

When it comes to financial data for stress testing, there’s a good news-bad news aspect. The good news may be that a bank did not suffer severe financial stress but the bad news is that it will be harder for the bank to model “bad events” if it does not have such data. And banks “will get written up if [the regulators] don’t believe their bad events,” said Tara Heusé Skinner, Manager at SAS Risk Research & Quantitative Solutions, and co-author of The Bank Executive’s Guide to Enterprise Risk Management. She was the first presenter of two at the May […]

Towards Reducing Systemic Risk

Have the risks posed by financial derivatives in the context of the current, still evolving, regulatory landscape been properly addressed? Michael Piracci, Director of PCB Compliance at Barclays, said that nowadays he has “a lot of interactions day-to-day with the clearinghouse” and overall, “it makes me feel a little more comfortable there’s a good system in place.” Piracci was the first of four presenters at a webinar titled Derivatives Regulatory Update held on March 31, 2015, sponsored by the Global Association of Risk Professionals. Piracci began by explaining the role of the Central Counterparty (CCP) and the Futures Commission Merchants […]

Tailoring Risk Model to Investment Strategy

Due to the growing complexity of measuring financial risk, “risk has become a patchwork” of different models, said Phil Jacob, Senior Director at Axioma Risk Research. He was the sole presenter in a webinar about tailoring the right risk model to your investment strategy held on March 4, 2015, and sponsored by the Global Association of Risk Professionals (GARP). Jacob identified four inherent challenges. “There are operational issues stemming from existing rigid approaches,” leading to “difficulty in aggregating risk.” There is a lack of consistency in modeling portfolios, which can run the gamut from very simple proxies all the way […]

Alternative Mutual Funds 2

“SEC’s mission is to protect investors and support responsible capital formation,” said Raymond Slezak, Assistant Regional Director at the Securities and Exchange Commission (SEC). He was the second of three presenters at the GARP-sponsored webinar held February 17, 2015, on Alternative Mutual Funds: Risk Governance Under SEC Security. Liquid alternative mutual funds were “listed as a priority” as early as 2013, he said, because “any time there’s rapid growth” or “concern about the dynamics of money managers moving into an area,” it attracts SEC interest. As a metaphor about the regulatory thought about the new funds, Slezak repeated a quotation […]

Stress Testing Mortgages. Part 2

The team of Scott L. Smith, Jesse Weiher, and Debra Fuller at the Federal Housing Finance Agency (FHFA) use specialized financial models to estimate potential losses. They carried out empirical tests of countercyclical shocks using four different models of mortgage credit risk. This posting continues a February 4, 2015, presentation by Scott L. Smith to an audience of financial risk managers at Global Association of Risk Professionals (GARP). Two models were devised at FHFA, and two are commercially available credit models: one, called Black Knight (formerly LPS-AA), and the other called ADCO Loan Dynamics. The estimated losses were converted to a capital […]