A Good I.M. is Hard to Find

How does an investor stay on good terms with its investment manager firm (I.M.)? In the first half of his talk, Sidney Hardee, Managing Partner of Hardee Brothers, LLC., spoke about hiring and firing. In this, the second half, he comments on the search, fees, taxes, and complexity. He was the sole presenter at the one-hour webinar “Hiring and Firing Investment Managers” sponsored by the Chartered Financial Analysts Institute on January 15, 2020. Search Hardee distilled the search for the correct I.M. down into four questions. How will I identify good investment managers? How much will it cost to gain exposure? […]

Grown-ups in strategic positions

How does an investor approach the problems of hiring and firing the investment manager firm (I.M.)? “In general, the first thing is to understand who you are as a business,” advises Sidney Hardee, Managing Partner of Hardee Brothers, LLC. “You must understand this thoroughly before engaging an investment manager.” He was the sole presenter of the one-hour webinar “Hiring and Firing Investment Managers” sponsored by the Chartered Financial Analysts Institute on January 15, 2020. Characteristics of the I.M. What are the characteristics of a good investment manager firm? Organizational stability is key, Hardee said. “What is the structure of this organization, […]

Shifting Energy Markets

How are strategic priorities in energy markets shifting? What are the risk management implications? “Geopolitical risks have worsened and technological innovation is causing more disruption,” said Medy Agami, senior partner and vice-chairman at Ben-Roz and Associates and co-founder of the consulting firm Opimas. He was the sole presenter of the webinar “Energy Market Strategy and Risk Playbook: How to prosper amid a wave of disruptive innovation, geopolitical uncertainty, market volatility & exponentially growing risk landscape in 2018 & beyond” sponsored by the Global Association of Risk Professionals (GARP) on August 7, 2018. “There are five main forces acting on fundamentally shifting markets,” […]

Early Warning Signs

“Overall, the energy sector remains stressed,” said Irina Baron, Associate Director at Moody’s Analytics. Baron was the third and final panellist discussing new dynamics in the handling of financial risk management in the energy sector at a webinar sponsored by the Global Association of Risk Professionals on November 29, 2017. Based on expected default frequency (EDF), 75 percent of US publicly-traded companies in the energy sector are not investment-grade risks. “Agency ratings give us a sense of which firms are more likely to default,” she noted. The drawback is that the realized default rate cannot be forecast. However, the expected […]

Managing Risk in Volatile Sector

Market observers have conflicting expectations, especially in the highly changeable energy sector. How can a talented analyst stay on top of it? Mehna Raissi, Senior Director at Moody’s Analytics, was the second of three panellists discussing new dynamics in the handling of financial risk management in the energy sector at a webinar sponsored by the Global Association of Risk Professionals on November 29, 2017. “Between 2008 and 2013, we were worried about rising oil prices,” Raissi said. However, “in the second half of 2014, oil prices came down and the headlines read: Recession caused by low oil prices.” Oil prices […]

New Dynamics in Energy Sector

How can financial risk be measured and managed in a volatile industry such as the energy sector? What are some of the common industry challenges? Due to low commodity prices and technological changes in the industry, there are new dynamics in the handling of financial risk management in the energy sector. Three speakers addressed specific changes in a webinar sponsored by the Global Association of Risk Professionals on November 29, 2017. “Sometimes the things we think we know, we don’t,” said Gordon Goodman of NRG Energy, the first of three speakers at the webinar. Goodman’s claim to fame is publication […]

Volatility Clustering

When looking at stock market time series, one notices immediately a certain “jitter” or “noise” in the daily returns. This is ordinary volatility. Every once in a while, volatility becomes higher and stays that way—for a while. “Volatility clustering occurs when the volatility of the returns becomes correlated from one day to another,” said Attilio Meucci, CEO and founder of Advanced Risk and Portfolio Management (ARPM). He was the sole presenter at the May 11, 2017, webinar on Modeling and Forecasting Volatility Clustering sponsored by the Global Association of Risk Professionals. Meucci began by showing an example of volatility clustering […]

Currency Option Trading Strategies

Throughout 2015 currency volatility has been increasing, even among established currencies such as the Swiss franc. Persistent exchange rate volatility can be an especially serious problem for currencies of emerging economies. Central banks often intervene by using foreign exchange reserves to purchase and sell foreign currency directly in the spot market. This relies on the continuous accumulation of foreign exchange reserves, which may be very difficult for emerging economies. How, then, can the central banks of such nations best manage currency fluctuations? In 2007-8, when the Colombian peso exchange rate was volatile, the Colombian central bank tried various strategies in […]

When Data Is Sparse. Part 2

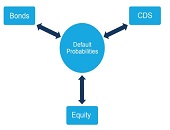

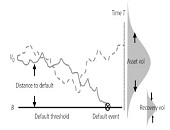

It’s difficult to model sovereign credit risk for emerging markets using structural models such as the Merton model because “calibration is always an issue,” said Rob Stamicar, Senior Director of Research in Multi-Asset Class Risk Management at Axioma, continuing a theme during the second half of his webinar on December 2, 2014. During the first half, he showed how the probability of default can be used as a common link among the asset classes of interest (bonds, swaps, and equities). In the second half, he focused more on sovereign credit risk. Calculation of sovereign risk could be done directly, “but […]

When Data Is Sparse. Part 1

When modelling risk in emerging markets, are you hampered by sparse data? “Relationships between different asset classes can help measure the sovereign risk in emerging markets,” said Rob Stamicar, Senior Director of Research in Multi-Asset Class Risk Management at Axioma. He was sole presenter at a webinar on December 2, 2014, sponsored by the Global Association of Risk Professionals. When modelling global multi-asset class portfolios, “aggregation can be challenging,” said Stamicar, because the FX rates must also be taken into consideration—the subject for another day. His talk focussed on three asset classes: equity, fixed income, and credit portfolios. Infrequent data, […]